Are Traditional Payment Processors Dead? The Truth About Web3 Global Payments in 2026

![Writer: [[[Free!!]<<<<]] Watch: 스포르팅 - 토트넘 Live Stream 13 September 2022](https://lh3.googleusercontent.com/a/AItbvmktwQc0wCdd3ZEETSYItRQubwwBzOyjD_dcigRf=s96-c)

They're Not Dead: They're Desperate

Here's what nobody's telling you.

Traditional payment processors aren't dying. They're frantically integrating Web3 to stay alive.

Stripe acquired Bridge for $1.1 billion in February 2025. Visa now settles payments with PayPal's PYUSD across 40+ markets. Mastercard's Multi-Token Network generated $2 billion in annualized volume from crypto cards alone.

The old guard sees what's coming. They're building lifeboats while the ship sinks.

But here's the real question: Why copy their outdated infrastructure when you can leapfrog entirely?

The $14,500 Monthly Problem

Run the numbers on traditional credit card processing.

2.5-3.5% per transaction plus flat fees. For a business processing $500,000 monthly, that's $14,500 in fees. Every single month.

Web3 global payments? Sub-1% costs with instant settlement. Gas fees for that same $500,000? Approximately $100.

That's a 99.3% reduction in payment processing costs.

Not 10%. Not 50%. Ninety-nine percent.

Monthly stablecoin payment flows exceeded $10 billion in early 2026. Business transactions represent 63% of total volume. The blockchain payments market hit $3.2 billion in 2023 and projects to reach $81.5 billion by 2030.

This isn't speculation anymore. It's operational infrastructure.

Why NOWPayments and CoinPayments Fall Short

Most merchants exploring crypto payments default to NOWPayments or CoinPayments. Familiar names. Established platforms.

Here's what they don't tell you:

Custodial control. Both platforms hold your funds. You're trading Visa's custody for another middleman's custody. That's not Web3: that's Web2 with crypto paint.

Limited stablecoin options. They support dozens of volatile cryptocurrencies but lack deep integration with truly stable assets like LUSD.

No NFT receipt infrastructure. Your accounting department still downloads CSV files like it's 2015.

Recurring fees. Lower than credit cards, sure. But why pay any processing fees when self-custody merchant accounts exist?

Triple-A offers better stablecoin support but still operates on custodial rails. You don't own your payment infrastructure. You rent it.

That's the fundamental difference between copying Web3 and being Web3.

Self-Custody Merchant Accounts: The Real Revolution

Here's where Larecoin diverges from every NOWPayments alternative on the market.

Self-custody from day one. Your private keys. Your funds. Your control.

No intermediaries holding your revenue. No surprise account freezes. No waiting 3-5 business days for settlements that should be instant.

Traditional processors: and most crypto payment gateways: operate on trust. You trust them to hold your money, process your transactions, and eventually release your funds.

Self-custody eliminates trust requirements entirely. Smart contracts execute automatically. Payments settle on-chain. You maintain complete financial sovereignty.

This isn't just philosophical. It's practical financial engineering for businesses tired of begging banks for access to their own money.

The LUSD stablecoin benefits become obvious immediately. Decentralized. Overcollateralized. No centralized issuer controlling your business operations.

While Circle or Tether can freeze USDC or USDT at government request, LUSD operates entirely on-chain through smart contracts. Your receivables token can't be seized, frozen, or controlled by any central authority.

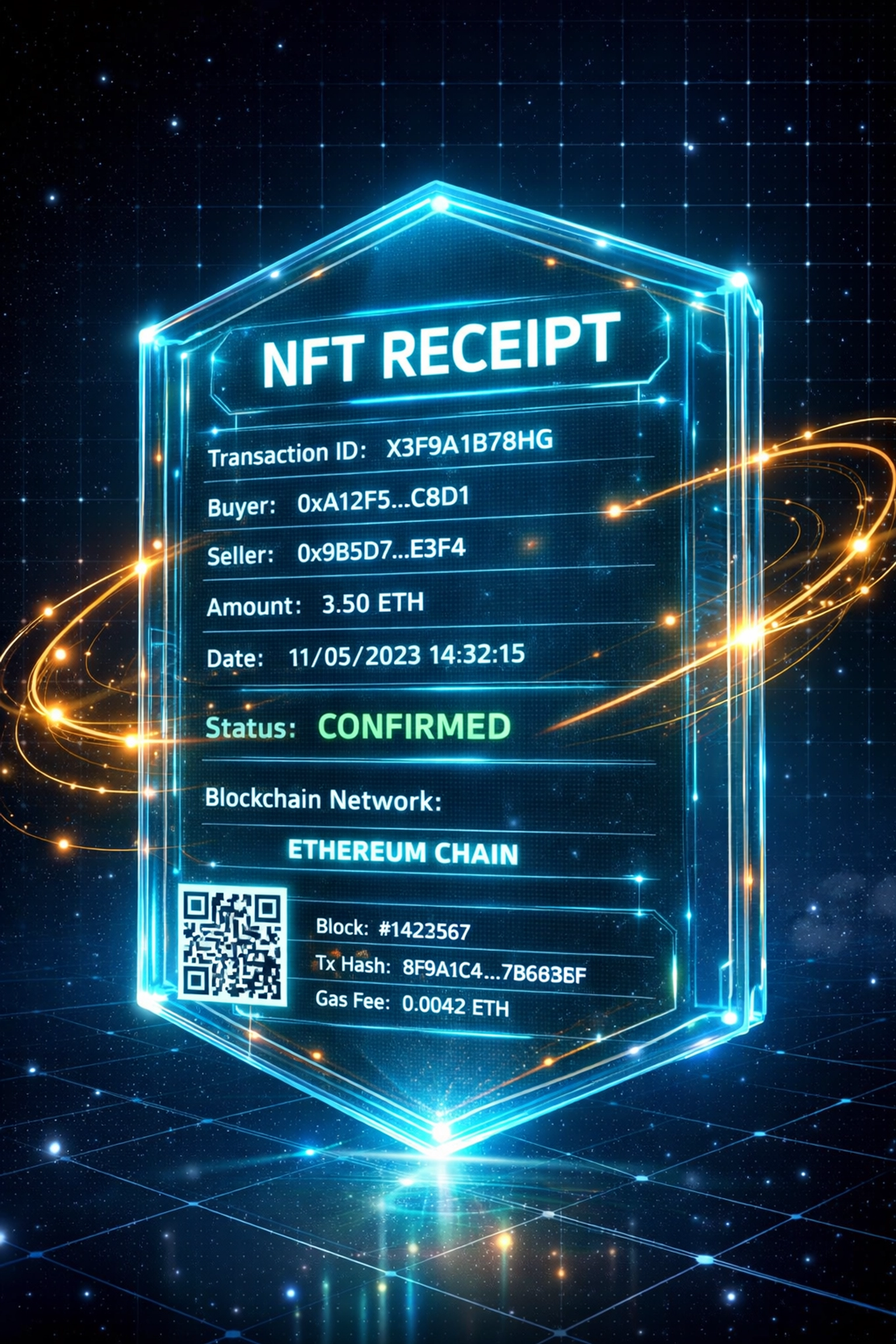

NFT Receipts for Accounting: No More Spreadsheet Hell

Every accountant's nightmare: reconciling payment processor statements with actual inventory.

Stripe says you sold 847 items. Your inventory shows 849. Was it a refund? A chargeback? A processing error?

Now multiply that confusion across multiple payment processors, currencies, and sales channels.

NFT receipts for accounting solve this permanently.

Every transaction mints a unique NFT receipt. Immutable. Time-stamped. Containing complete transaction metadata.

Item purchased

Price paid

Payment method

Customer wallet address

Exact timestamp

Associated smart contract

Your accounting software queries the blockchain directly. Zero reconciliation errors. Zero missing receipts. Zero "the payment processor says something different than our internal records" conversations.

This is what real Web3 infrastructure looks like. Not just accepting crypto payments: fundamentally reimagining how business transactions work.

The Receivables Token Nobody's Talking About

Here's the feature that makes traditional payment processors obsolete overnight.

Receivables tokens.

You accept a payment. Instead of waiting for settlement, you receive a tokenized receivable instantly. That token represents the payment obligation and can be:

Held until settlement

Sold on secondary markets for immediate liquidity

Used as collateral for DeFi lending

Transferred to suppliers as payment

Traditional factoring companies charge 2-5% to advance payment on invoices. Receivables tokens let you access that liquidity instantly at minimal cost.

Small businesses no longer choose between cash flow and profitability. The payment becomes immediate liquidity.

Crypto POS System for Small Business: Beyond Online

Most discussions about Web3 global payments focus on e-commerce.

What about brick-and-mortar?

Larecoin's crypto POS system for small business handles in-person transactions with the same efficiency as online payments.

Customer walks in. Scans QR code. Payment settles instantly. NFT receipt generates automatically.

No card readers. No merchant accounts. No monthly terminal fees. No PCI compliance headaches.

Gas-only transfers mean the only cost is network fees: typically under $0.50 per transaction regardless of payment size.

Compare that to traditional interchange fees that scale with transaction value. Selling a $5,000 item? Credit cards take $125-175. Gas fees? Still under $1.

The Bank-Free Business Reality

February 2026 marks three years since Operation Chokepoint 2.0 intensified banking pressure on crypto businesses.

Thousands of legitimate companies lost banking access overnight. Not for fraud. Not for illegal activity. Simply for operating in cryptocurrency.

Web3 global payments eliminate banking dependencies entirely.

Your business doesn't need:

A merchant account

A business checking account

Payment processor approval

Bank permission to operate internationally

You need:

A wallet

An internet connection

Smart contracts

That's financial sovereignty. Not the theoretical kind discussed at conferences. Practical, operational independence from banking infrastructure that can deplatform you arbitrarily.

What Traditional Processors Will Never Admit

Visa's stablecoin-linked card spending quadrupled year-over-year. That's validation.

But it's also admission.

Traditional rails can't compete on cost, speed, or global accessibility. So they're bolting crypto capabilities onto 1970s infrastructure and hoping merchants don't notice the fundamental limitations.

Stripe directing 20% of leading AI firms' payments through stablecoins isn't innovation. It's surrender.

They see the efficiency gains. They understand the cost reduction. They're desperately trying to stay relevant by becoming crypto payment facilitators instead of traditional processors.

The 2026 Decision Point

You can stick with traditional payment processors integrating crypto as a feature.

Or you can build on native Web3 infrastructure from day one.

One approach reduces your fees from 3% to 1.5%. The other reduces them to sub-0.1%.

One gives you faster settlement. The other gives you instant settlement and complete financial control.

One offers crypto payment acceptance. The other reimagines your entire business operations around self-custody, NFT receipts, and receivables tokens.

Traditional payment processors aren't dead. But their business model is terminal.

The question isn't whether Web3 global payments will replace legacy infrastructure. It's whether your business embraces that transition now or spends the next three years paying premium fees to middlemen managing their decline.

Choose accordingly.

Ready to slash merchant interchange fees by 99%?Explore Larecoin's self-custody merchant solutions and join the businesses already operating bank-free in 2026.

Comments