The Receivables Token Revolution: How Larecoin Merchants Accept Crypto, Defer Taxes, and Keep 100% Custody

- [[[Free!!]<<<<]] Watch: 스포르팅 - 토트넘 Live Stream 13 September 2022

- Feb 20

- 4 min read

![Writer: [[[Free!!]<<<<]] Watch: 스포르팅 - 토트넘 Live Stream 13 September 2022](https://lh3.googleusercontent.com/a/AItbvmktwQc0wCdd3ZEETSYItRQubwwBzOyjD_dcigRf=s96-c)

Welcome to True Financial Sovereignty

Merchants are done getting crushed by 2.9% + $0.30 transaction fees.

Done trusting third parties with their funds.

Done converting crypto immediately because platforms demand it.

Larecoin's receivables token model flips the entire script. Merchants accept crypto. Keep 100% custody. Defer taxes. Pay gas-only fees.

This isn't incremental improvement. It's a complete structural overhaul of how Web3 payments work.

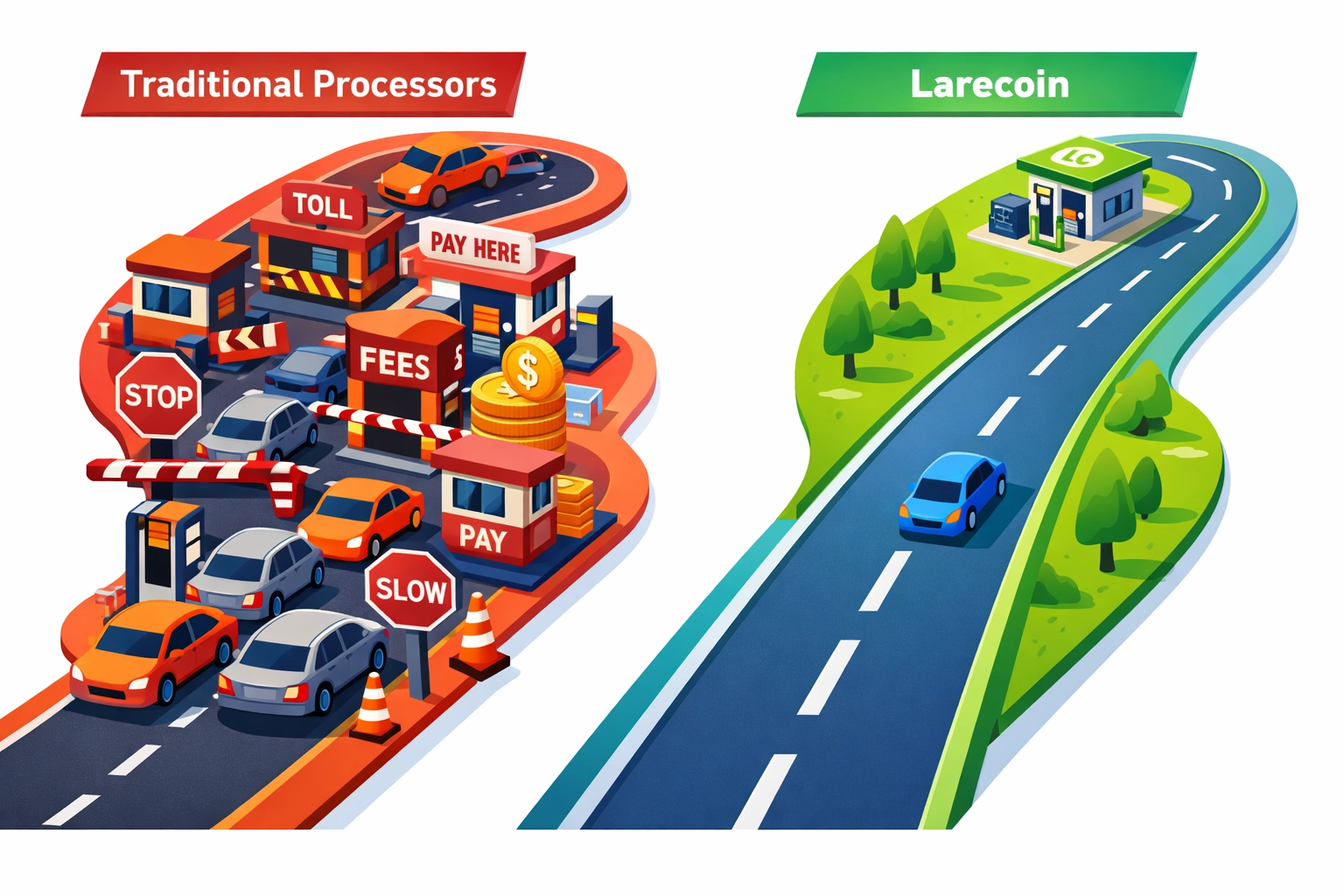

The Problem With Traditional Crypto Payment Processors

NOWPayments and CoinPayments follow the old playbook. They hold your funds. They control conversion timing. They charge platform fees on top of network fees.

You're basically renting permission to accept crypto.

Larecoin merchants? They own the entire payment infrastructure from day one.

How Receivables Tokens Actually Work

Think of receivables tokens as digital IOUs that merchants control completely.

Customer pays in crypto. Transaction creates an on-chain receivable. Merchant's wallet receives it instantly. Zero intermediaries touching the funds.

The receivable sits in your wallet as a tokenized asset. You decide when to convert. You decide when to claim. You maintain custody through every step.

Traditional processors force instant conversion. Larecoin gives you time sovereignty.

The Three-Step Merchant Onboarding Process

Forget 5-day approval processes and minimum transaction requirements.

Step 1: Create your LareBlocks wallet Step 2: Add LARE/LUSD addresses to your checkout Step 3: Start accepting receivables tokens

Total time? Under 10 minutes.

No credit checks. No monthly minimums. No waiting for platform approval.

Your wallet. Your rules. Your timeline.

NFT Receipts: The Audit Trail Revolution

Every Larecoin transaction generates an immutable NFT receipt.

Permanently stored on-chain. Timestamped automatically. Linked to specific wallet addresses. Programmatically verifiable.

For merchants, this means:

Automatic audit trails without manual record-keeping

Dispute resolution with blockchain-verified proof

Tax documentation that's tamper-proof

Complete transaction history accessible forever

CoinPayments gives you CSV exports. Larecoin gives you cryptographic proof stored on Solana.

Tax Deferral: The Hidden Advantage

Here's where receivables tokens become genuinely revolutionary for merchant economics.

Receivables remain tax-free until converted to fiat. You can claim them as expenses. You control the conversion timing based on your tax strategy.

Compare this to NOWPayments' forced instant conversion model. Every transaction triggers an immediate taxable event. No flexibility. No optimization opportunities.

Larecoin merchants who understand tax strategy can defer obligations indefinitely while building crypto reserves.

Consult your tax professional obviously. But the structural advantage is massive.

The Master/Sub-Wallet Architecture

Security through custody. Not security through trust.

Larecoin's wallet architecture lets merchants create hierarchical permission structures:

Master wallet with full control

Sub-wallets for different employees or departments

Multi-signature support for team approvals

Hardware wallet integration for maximum security

NOWPayments controls your funds during processing. CoinPayments holds balances on your behalf.

Larecoin never touches your crypto. Ever. You're the sole keyholder.

The security model shifts from "trust the platform" to "verify the blockchain."

Fee Destruction: 0.25% vs 2.9% + $0.30

Traditional payment processors stack fees like a pyramid scheme.

Base rate: 2.9% Per-transaction: $0.30 Interchange: 1.5-3% Assessment: 0.1-0.2% Cross-border: +1-2%

Small merchants get destroyed. A $20 sale can lose $1.50 in fees. That's 7.5% gone instantly.

Larecoin's model? Gas-only transfers with 0.25% transaction fee.

That $20 sale? You keep $19.95.

Over 50% fee reduction on average. Sometimes 70%+ for international transactions.

LUSD Stablecoin: Volatility Insurance Without Custody Loss

Merchants love crypto. Merchants hate price swings during settlement.

LUSD (Larecoin USD) solves this completely.

Accept payments in volatile crypto. Instantly convert to LUSD at settlement. Maintain stablecoin reserves in your wallet. Convert back to LARE or other crypto whenever you want.

You get price stability without surrendering custody to a platform.

CoinPayments forces fiat conversion to stabilize. NOWPayments requires platform-held stablecoin balances.

LUSD stays in your wallet. Always.

Instant Swaps Across 55+ Cryptocurrencies

Payment flexibility isn't about accepting every token imaginable.

It's about converting what you accept into what you want to hold.

Larecoin supports instant on-demand swaps with:

Bitcoin

Ethereum

Solana

USDC/USDT

50+ additional major cryptocurrencies

Customer pays in whatever they prefer. You receive in whatever you prefer. The receivables token model handles conversion automatically if you configure it.

Or keep everything as received. Your choice entirely.

Regulatory Compliance: The CLARITY Act Framework

The CLARITY Act (H.R. 3633) passed the House in July 2025.

It classified Larecoin's receivables token as a digital commodity under CFTC oversight. Not an SEC-regulated security.

Translation? Clear compliance pathways without securities registration nightmares.

Merchants operating with Larecoin aren't navigating regulatory grey zones. The framework exists. The classification is defined.

This matters enormously for businesses concerned about future enforcement actions.

Real-World Merchant Math

Let's run actual numbers.

Online retailer doing $100K monthly revenue:

Traditional processor fees: $3,200 ($2,900 + $300 flat fees + interchange) Larecoin fees: $250 Monthly savings: $2,950 Annual savings: $35,400

International business with 40% cross-border transactions:

Traditional processor fees: $4,800 (additional 1.5% cross-border premium) Larecoin fees: $250 Monthly savings: $4,550 Annual savings: $54,600

These numbers aren't hypothetical. They're structural differences in how receivables tokens eliminate intermediary extraction.

The Custody Question That Defines Everything

Every Web3 payment decision comes down to one question:

Who holds the keys?

NOWPayments: They do during processing CoinPayments: They do for balance storage Larecoin: You do from transaction to conversion

Self-custody isn't a feature. It's the fundamental architecture that makes everything else possible.

Tax deferral only works if you control conversion timing. Fee reduction only matters if platforms can't extract custody premiums. Financial sovereignty requires actual sovereign control of assets.

Larecoin's receivables token model makes custody the default, not the premium tier.

Why Competitors Can't Replicate This

NOWPayments and CoinPayments are built on custodial architectures.

Their business models require holding merchant funds to generate revenue. They earn interest on float. They charge conversion fees. They monetize custody.

Switching to true self-custody would destroy their revenue structure.

Larecoin started with non-custodial as the foundation. Everything else built on top of that core principle.

You can't bolt financial sovereignty onto a platform designed around extraction.

Getting Started: The Practical Steps

Ready to accept crypto with full custody and zero platform control?

Visit larecoin.com and download the LareBlocks wallet.

Set up your LARE and LUSD addresses.

Add them to your checkout process.

Start receiving receivables tokens.

No applications. No approval delays. No monthly commitments.

The receivables token revolution isn't coming. It's live right now.

Join the merchants who've already made the switch. Keep your custody. Defer your taxes. Slash your fees.

Welcome to Web3 payments that actually put merchants first.

Comments