7 Mistakes You're Making with Merchant Interchange Fees (and How Larecoin Fixes Them)

- [[[Free!!]<<<<]] Watch: 스포르팅 - 토트넘 Live Stream 13 September 2022

- Feb 22

- 4 min read

![Writer: [[[Free!!]<<<<]] Watch: 스포르팅 - 토트넘 Live Stream 13 September 2022](https://lh3.googleusercontent.com/a/AItbvmktwQc0wCdd3ZEETSYItRQubwwBzOyjD_dcigRf=s96-c)

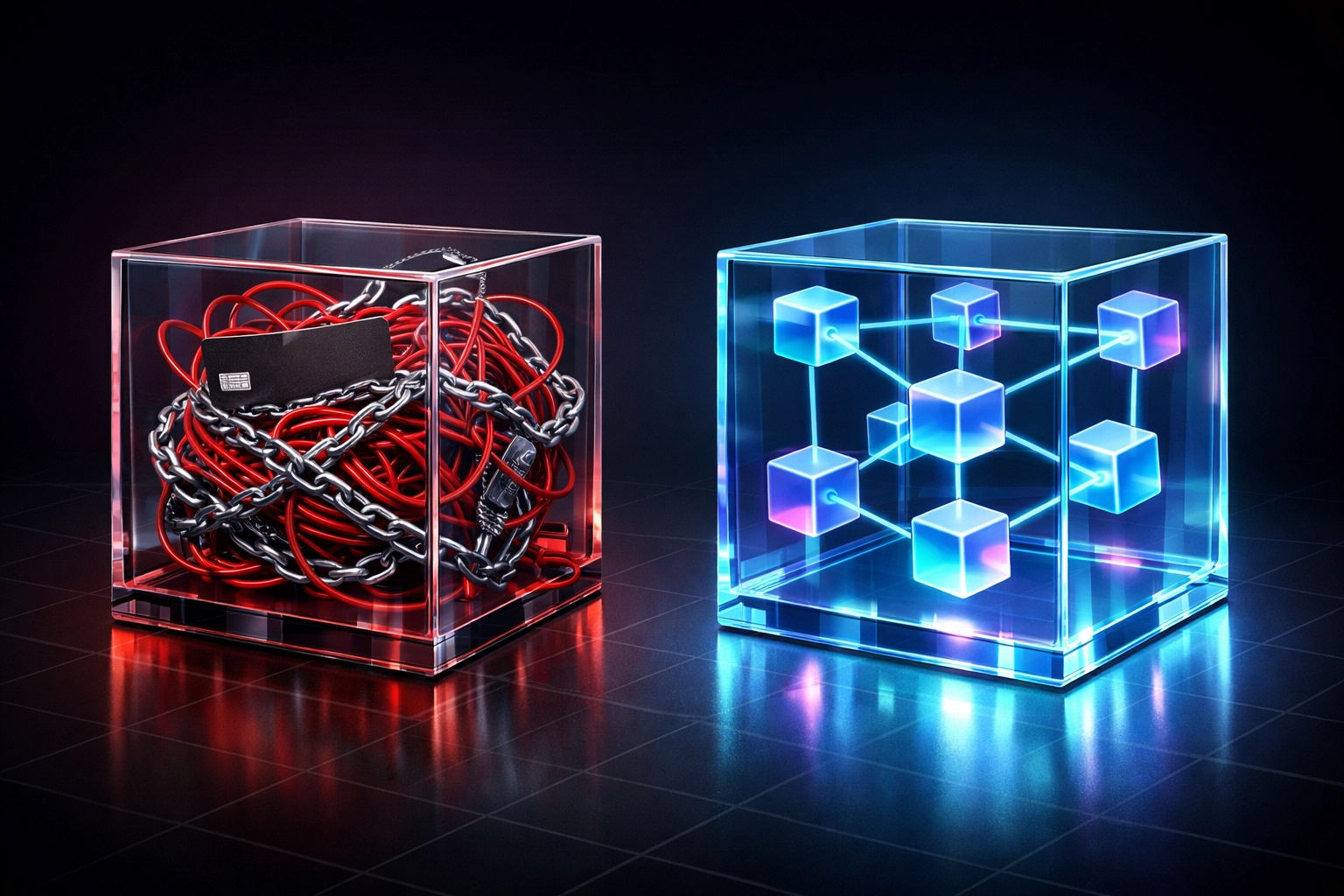

You're bleeding money on interchange fees.

Every swipe. Every tap. Every online checkout. Traditional payment processors are quietly draining 2-3% of your revenue while hiding the real costs in fine print.

Here's the thing: Web3 already solved this problem. You just haven't switched yet.

Let's break down the 7 biggest mistakes merchants make with interchange fees, and how Larecoin's Web3 payment infrastructure eliminates them entirely.

Mistake #1: Accepting "Interchange Plus" Pricing at Face Value

Traditional processors love the "Interchange Plus" pitch. Sounds transparent, right?

Wrong.

They quote you +0.15% + $0.10 markup. Looks competitive. But buried in pages of terms and conditions? Hidden surcharges. Interchange padding. Monthly minimums. Gateway fees. Statement fees.

Your "competitive rate" balloons to 2.8% before you even blink.

The Larecoin Fix: No markup games. No hidden processors. Just straight blockchain transactions with minimal gas fees. You see exactly what you pay, usually under 0.5% in total costs. Self-custody means no middleman taking a cut. Your money stays your money.

Mistake #2: Paying for Interchange Padding You Can't Even See

Here's a dirty secret: Some payment processors add phantom "interchange fees" to your statement that never actually go to Visa or Mastercard.

They're pocketing the difference.

You can't catch it without comparing your statements line-by-line against current interchange rate tables. Who has time for that?

The Larecoin Fix: Blockchain transactions are immutable and transparent. Every fee is visible on-chain. No processor markup. No padding. Just verifiable, cryptographic proof of exactly where your money goes. Compare that to NOWPayments or CoinPayments charging 0.5-1% processor fees on top of network costs.

Mistake #3: Losing Money on Transaction Misclassification

Card-present transaction accidentally coded as card-not-present? Congratulations, you just triggered a higher interchange tier.

For a business processing $100,000 monthly, this one mistake adds $500-$1,000 in unnecessary fees. Every. Single. Month.

The Larecoin Fix: Web3 payments don't have "card-present" vs. "card-not-present" classifications. Crypto transactions cost the same whether customers pay in-store via contactless POS or online through your merchant portal. One unified rate. No downgrades. No qualification tiers.

Plus: Every transaction generates an NFT receipt. Immutable proof of purchase with complete transaction metadata. Better than any legacy receipt system.

Mistake #4: Getting Stuck with the Wrong Merchant Category Code

Set up your merchant account wrong? Your MCC determines your interchange rates forever.

Restaurants pay different rates than retail. Nonprofits get special treatment. E-commerce businesses get hammered.

One checkbox during onboarding costs you thousands annually.

The Larecoin Fix: Blockchain doesn't care about your business category. Same fees for restaurants, retailers, service providers, NFT marketplaces, metaverse shops, everyone. The decentralized network treats all merchants equally.

And with Larecoin's rigorous US compliance framework (MSB registration + state MTL licensing strategy), you get Web3 innovation with regulatory legitimacy. No "offshore processor" risks.

Mistake #5: Triggering Downgrades Through Settlement Delays

Batch your transactions tomorrow instead of today? Downgrade.

Miss the settlement window? Downgrade.

Technical glitch delays processing? Downgrade.

Each downgrade pushes you into higher interchange tiers. Death by a thousand cuts.

The Larecoin Fix: Blockchain settlement happens in real-time. No batch processing. No settlement windows. Transactions confirm in seconds. Your funds move instantly to your self-custody wallet. No bank holds. No clearing delays. Just immediate, final settlement.

LUSD stablecoin version available for merchants who want price stability without volatility. Get crypto's speed with dollar stability.

Mistake #6: Ignoring Debit Card Routing Optimization

Different debit networks charge different rates. Routing matters.

But traditional processors rarely optimize routing for your benefit. Why would they? They profit from higher fees.

You leave money on the table because you don't even know routing is negotiable.

The Larecoin Fix: No debit networks. No routing decisions. Just direct peer-to-peer transactions on Solana's blazing-fast Layer 1 blockchain. Sub-second finality. Fraction-of-a-penny transaction costs.

Compare this to CoinPayments' clunky multi-coin routing or NOWPayments' network fees that vary wildly by blockchain. Larecoin optimizes for Solana's speed and cost efficiency.

Mistake #7: Overlooking Hidden Network Assessment Fees

Beyond interchange, card networks charge "assessment fees." And "brand fees." And "network authorization fees." And about fifteen other micro-charges.

Your statement becomes a novel.

You pay them all without even understanding what they mean.

The Larecoin Fix: One blockchain. One transparent fee structure. Gas fees visible upfront. No surprise charges three statements later. The entire Larecoin ecosystem, from swap and bridge to merchant portal to NFT marketplace, operates on the same predictable cost model.

Self-custody wallets mean you control when and how you move funds. No forced fee structures. No network assessment surprise bills.

The Web3 Payments Advantage: Real Numbers

Traditional processing: 2.5-3.5% + $0.30 per transaction NOWPayments/CoinPayments: 0.5-1% + network fees (varies wildly) Larecoin: Gas fees only (typically <0.1%) + optional LUSD stablecoin features

For a merchant processing $50,000 monthly:

Traditional: ~$1,400 in fees

NOWPayments: ~$250-500 (depending on crypto network)

Larecoin: ~$50-100 in total costs

That's $15,000+ saved annually. Just by switching payment rails.

Compliance Meets Innovation

Here's where Larecoin separates from offshore crypto processors playing regulatory roulette.

Full MSB (Money Services Business) registration. State-by-state MTL (Money Transmitter License) compliance strategy. Not cutting corners. Not hoping regulators don't notice.

Building the compliant Web3 payment infrastructure the industry desperately needs.

You get crypto's cost savings without the regulatory nightmares keeping your legal team up at night.

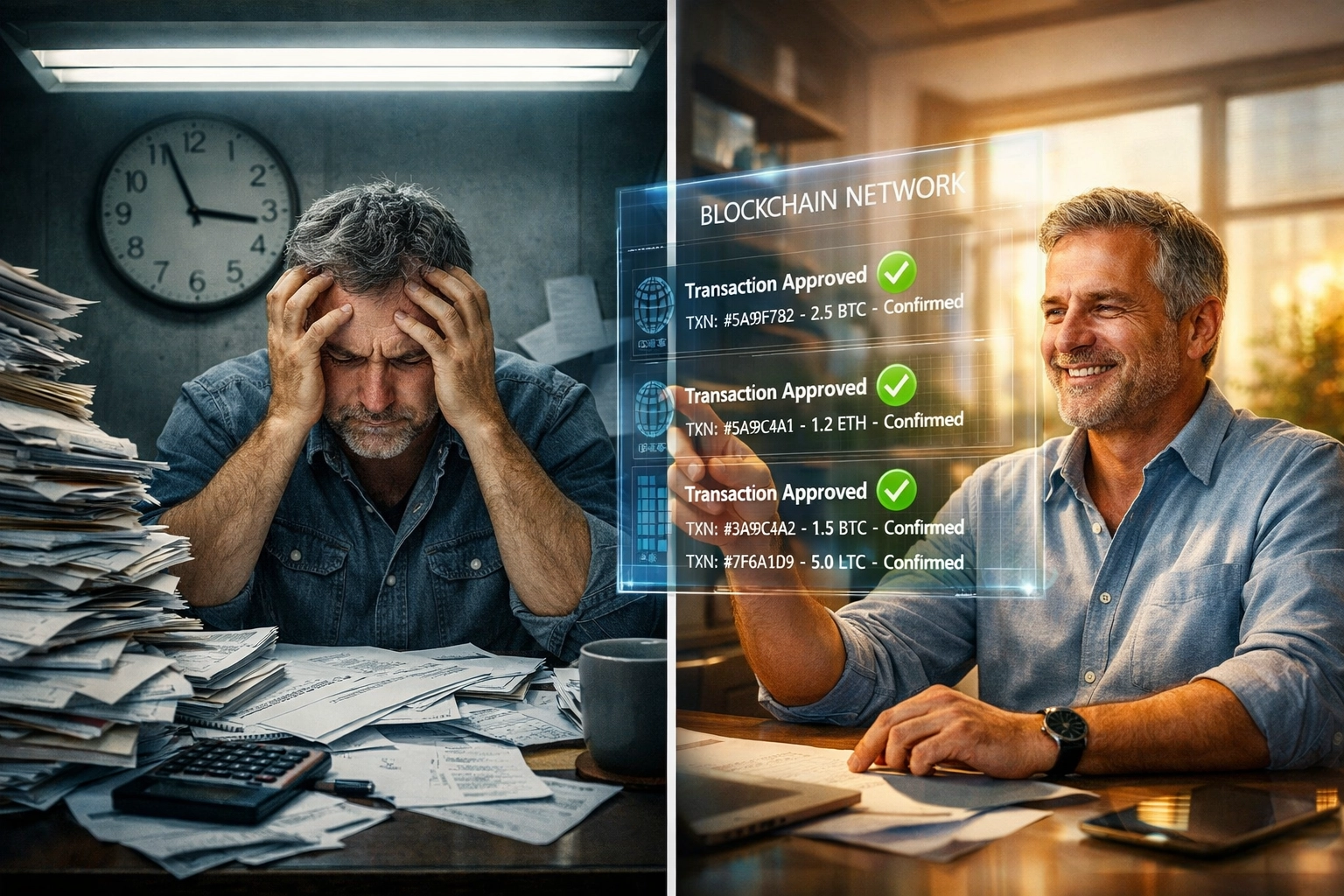

Stop Overpaying. Start Building.

Interchange fees are a legacy system tax.

You're paying for infrastructure built in the 1970s. Card networks. Issuing banks. Acquiring banks. Payment processors. Gateway providers. Each taking their cut.

Web3 collapsed that entire stack into peer-to-peer transactions.

Larecoin built the merchant tools to make it seamless. Contactless POS for in-store. Merchant portal for e-commerce. NFT receipts for customer engagement. LUSD for price stability. Self-custody for complete control.

The infrastructure is live. The fees are transparent. The savings are real.

Your competitors are already switching.

Question is: How much longer can you afford to overpay?

Ready to eliminate interchange fees? Explore the Larecoin ecosystem and join the Web3 payments revolution. This is post #42 in our 100-post marathon documenting how crypto is solving real-world merchant problems.

Want the deep dive? Check out our ultimate guide to reducing merchant interchange fees.

The future of payments isn't coming.

It's here.

Comments