How the CLARITY Act (H.R. 3633) Makes Larecoin the Smarter Receivables Token in 2026

- [[[Free!!]<<<<]] Watch: 스포르팅 - 토트넘 Live Stream 13 September 2022

- Feb 12

- 4 min read

![Writer: [[[Free!!]<<<<]] Watch: 스포르팅 - 토트넘 Live Stream 13 September 2022](https://lh3.googleusercontent.com/a/AItbvmktwQc0wCdd3ZEETSYItRQubwwBzOyjD_dcigRf=s96-c)

Regulatory Clarity Just Changed Everything

The CLARITY Act passed. Digital commodities got legitimacy. Larecoin got classified exactly where it needed to be.

H.R. 3633 drew the line between securities and commodities in crypto. Larecoin landed squarely in commodity territory. That means CFTC oversight. Clear tax treatment. Predictable compliance frameworks.

No more regulatory limbo. No more merchant hesitation.

What CLARITY Act Recognition Actually Means

Digital commodity status under H.R. 3633 gives Larecoin three massive advantages:

Legal certainty - Merchants know exactly what they're accepting. Accountants know how to classify it. Tax treatment is standardized.

Banking access - Crypto commodity classification opens doors with payment processors and financial institutions that stayed away from gray-area tokens.

Long-term viability - Regulatory approval signals staying power. Businesses can build 5-year payment strategies around Larecoin without existential regulatory risk.

Compare that to platforms stuck in compliance limbo. NOWPayments and CoinPayments support hundreds of tokens, many with zero regulatory clarity. Merchants accepting those payments gamble on future classification.

The 50% Fee Savings Reality Check

Traditional payment rails bleed merchants dry.

Credit card processors: 2.9% + $0.30 per transaction. PayPal Business: 3.49% + fixed fee. International wire transfers: 3-5% plus currency conversion spreads.

Larecoin flips that model.

Gas-only transfers on LareBlocks Layer 1 cost fractions of a cent. No percentage-based fees. No intermediary taking a cut. Merchant receives 99.5% of payment value.

For a $10,000 B2B invoice:

Traditional processor: $290-$500 in fees

Larecoin: Under $5 in gas fees

That's not incremental savings. That's fundamental cost structure disruption.

The CLARITY Act made this legally viable at scale. Merchants can now route receivables through Larecoin without compliance headaches that historically justified legacy processor fees.

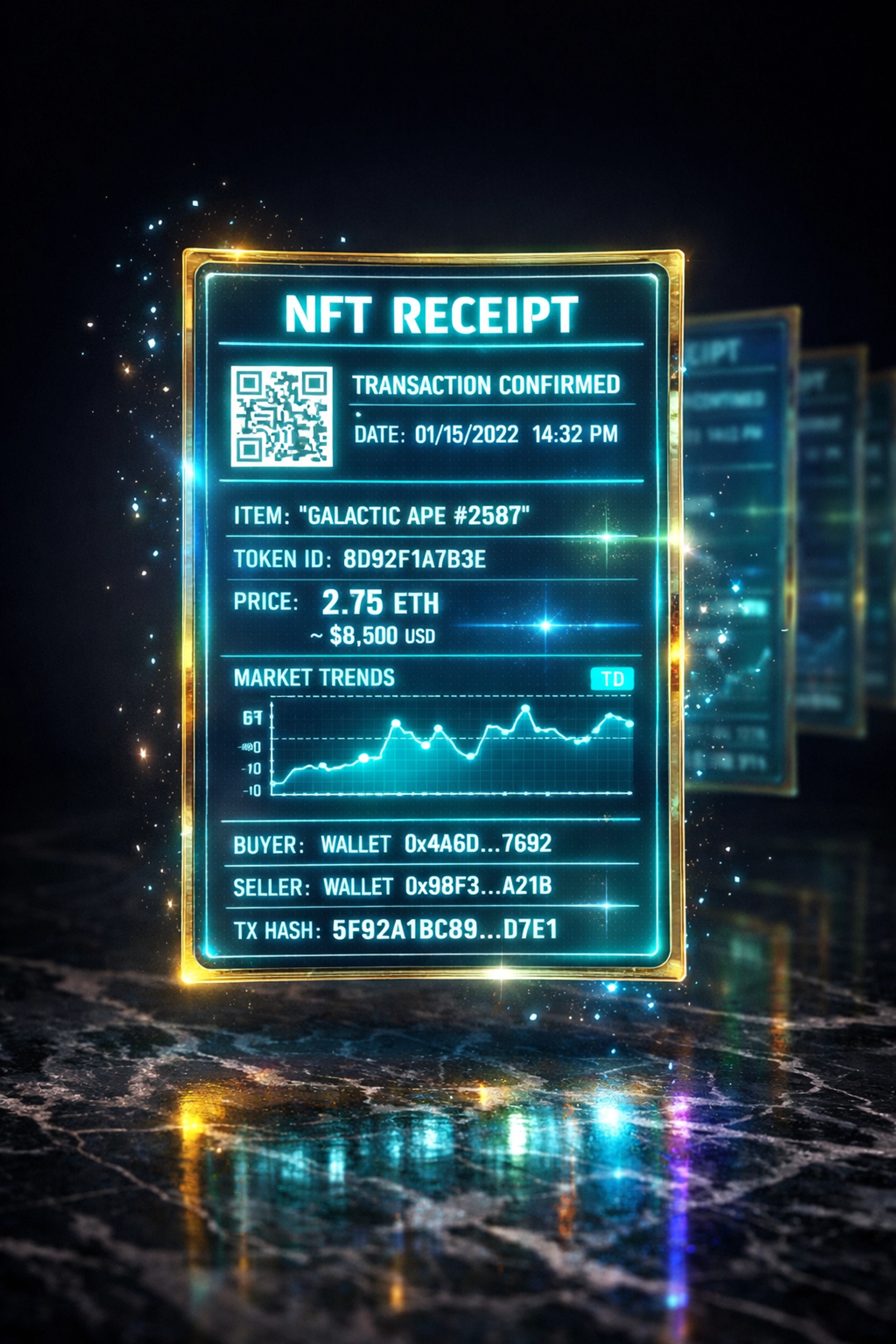

NFT Receipts: Proof of Payment Meets Utility

Every Larecoin transaction generates an optional NFT receipt.

Not a gimmick. A functional innovation.

These receipts live on-chain with immutable timestamp, amount, wallet addresses, and transaction metadata. They serve as:

Dispute resolution tools - Customer claims they never paid? The NFT receipt proves otherwise. Tamper-proof. Court-admissible in jurisdictions recognizing blockchain evidence.

Automated accounting - Integrate NFT receipt metadata directly into ERP systems. Reconciliation becomes automatic. No manual invoice matching.

Loyalty program foundation - Merchants can airdrop rewards to wallets holding specific receipt NFTs. Customer spent $1,000 last quarter? Their receipt NFTs qualify them for VIP perks automatically.

CoinPayments gives you a transaction ID. NOWPayments sends a confirmation email. Neither provides programmable, composable proof of payment with built-in utility layers.

Larecoin does.

LUSD Stablecoin: Volatility Solution Built In

Merchant objection #1 to crypto payments: "Bitcoin could drop 10% between customer payment and my bank deposit."

Valid concern. Wrong with Larecoin.

The LUSD stablecoin pegs 1:1 to USD within the Larecoin ecosystem. Merchants can:

Accept LARE (the native receivables token)

Auto-convert to LUSD at point of sale

Hold stable value until bank withdrawal

Zero volatility exposure. Zero separate stablecoin platform. Zero additional gas fees for conversion.

It's all native to the LareBlocks Layer 1 architecture. One ecosystem. One wallet. One compliance framework under CLARITY Act digital commodity classification.

Compare that to NOWPayments requiring manual conversion to third-party stablecoins. Or CoinPayments leaving merchants exposed to price swings between payment and settlement.

LareBlocks Layer 1: Security Through Self-Custody

Most crypto payment processors operate as custodians. Merchant funds sit in company-controlled wallets. That creates counterparty risk.

LareBlocks eliminates it.

Self-custody by default - Merchants control their own private keys. Larecoin never touches your funds. You're not trusting a payment processor's solvency.

Layer 1 native security - No bridge vulnerabilities. No wrapped token risks. Payments settle directly on LareBlocks mainnet with full validator decentralization.

CLARITY Act compliance built in - Digital commodity classification under H.R. 3633 requires clear custody disclosure. Larecoin's self-custody model exceeds those requirements by design.

When NOWPayments or CoinPayments hold merchant balances, they become targets. Custodial risk concentrates. LareBlocks distributes that risk to zero by making custody optional and self-directed.

AI-Powered Metaverse Shopping: The 2026 Edge

CLARITY Act legitimized crypto payments. Larecoin took it further.

The metaverse shopping layer integrates AI assistants that:

Analyze customer behavior - Purchase history, browsing patterns, wallet transaction data (with permission). AI recommends products before customers search.

Dynamic pricing - Real-time adjustments based on LARE token holder status, purchase volume, and loyalty tier. Smart contracts execute pricing automatically.

Virtual storefront optimization - AI tests thousands of store layout variations in metaverse environments. Merchants see which virtual displays drive highest conversion.

Traditional payment processors move money. Larecoin moves money and optimizes the entire purchase journey with AI.

Want to see it in action? Check out our full breakdown of metaverse shopping features launching this year.

The Competitor Reality: Why Others Fall Short

NOWPayments strengths: Wide token support, simple API integration. Weakness: No native stablecoin, no Layer 1 ownership, custodial model creates counterparty risk.

CoinPayments strengths: Established brand, merchant tools, fiat offramps. Weakness: High processing fees (0.5% still cuts margins), no AI features, no metaverse integration.

Both platforms offer payment processing. Neither offers an ecosystem.

Larecoin combines payment rails, stablecoin stability, NFT utility, AI optimization, and metaverse commerce in one CLARITY Act-compliant package.

That's not feature bloat. That's vertical integration for Web3 commerce.

February 2026: The Regulatory Tailwind

H.R. 3633 passed at the perfect moment.

Crypto winter ended. Institutions returned. Merchants needed legitimate payment solutions with regulatory backing.

Larecoin delivered exactly that.

Digital commodity classification removes the last barrier to mainstream merchant adoption. Banks can support it. Accountants can classify it. Regulators can approve it.

The 10-year marathon continues. But the CLARITY Act just shortened the distance to mass adoption significantly.

Getting Started Takes Minutes

Set up Larecoin merchant payments:

Create wallet at larecoin.com

Generate payment QR codes

Optional: Enable auto-convert to LUSD

Start accepting receivables with 50%+ fee savings

No lengthy approval process. No credit checks. No custodial agreements.

Self-custody means you're operational the moment your wallet syncs.

The regulatory clarity is here. The technology is live. The fee savings are real.

Smart merchants are already switching. The question isn't whether to adopt Larecoin: it's how quickly you can implement it before competitors gain the cost advantage.

Comments